风能、光伏、储能三辆马车齐头并进。

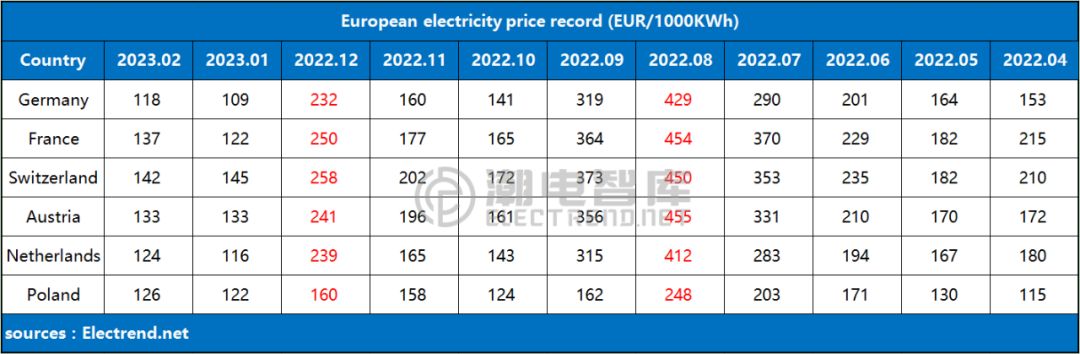

2022年,欧洲电价在8月和12月,共达到两次高峰值。

2022年3月至8月,欧洲电价一路走高,8月达到第一次峰值,期间德国电价翻了3倍以上,最高为429欧元/千度电。俄乌地缘冲突导致电力成本上升,欧洲没能及时应对供给中断的负面影响是主要原因。

9月至12月,欧洲各国电力政策电价初见成效,电价在10月回落至年初水平。但9月26日“北溪”管道被炸再次引起用电恐慌,电价转头向上一路涨至12月的第二次峰值。

2023年开始,欧洲能源转型初见成效,但欧盟在发展可再生能源产业上产生分歧:氢能和风能,被放到和太阳能同等高度的位置,导致可再生能源发展存在不协调的地方,电价反复起落也反映出欧洲能源发展的冲突性。

风能和太阳能(光伏),成为德国电力两大支柱,且比重逐年走高。

相比2010年,德国太阳能贡献值从18GW上升至60.6GW,比重从11%提升至26%;风能则是27GW升至64.5GW,占比从16%到27%。两大电力支柱在2022年的发电量,已超过德国年总量的50%。

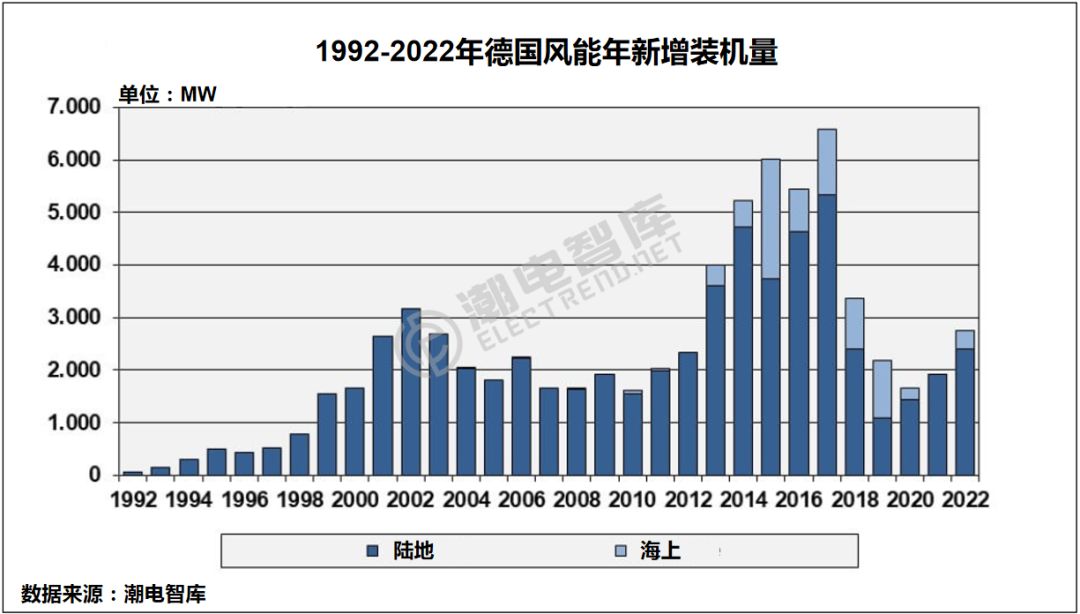

风能方面,2022年德国新增装机总量自2019年以来首次突破2.75GW,其中海上0.3GW,陆地2.4GW。

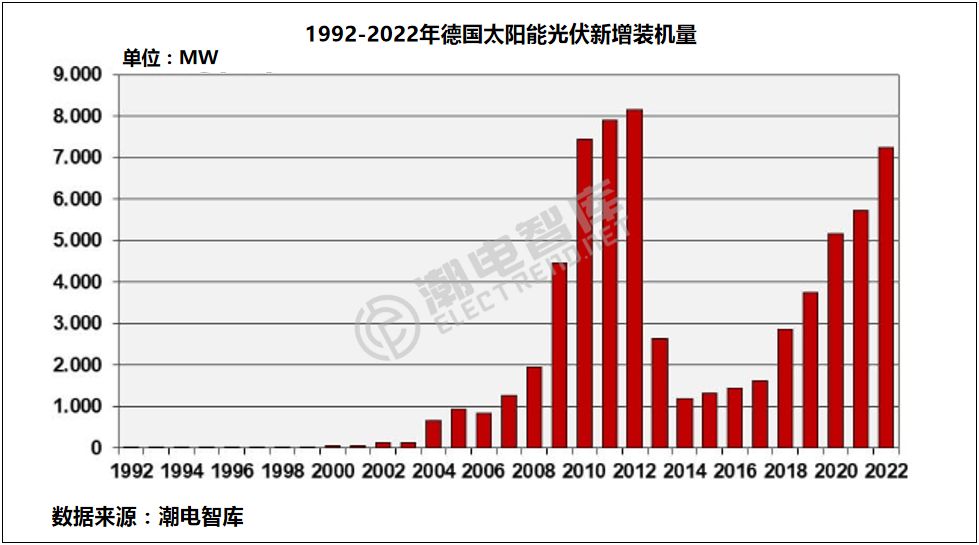

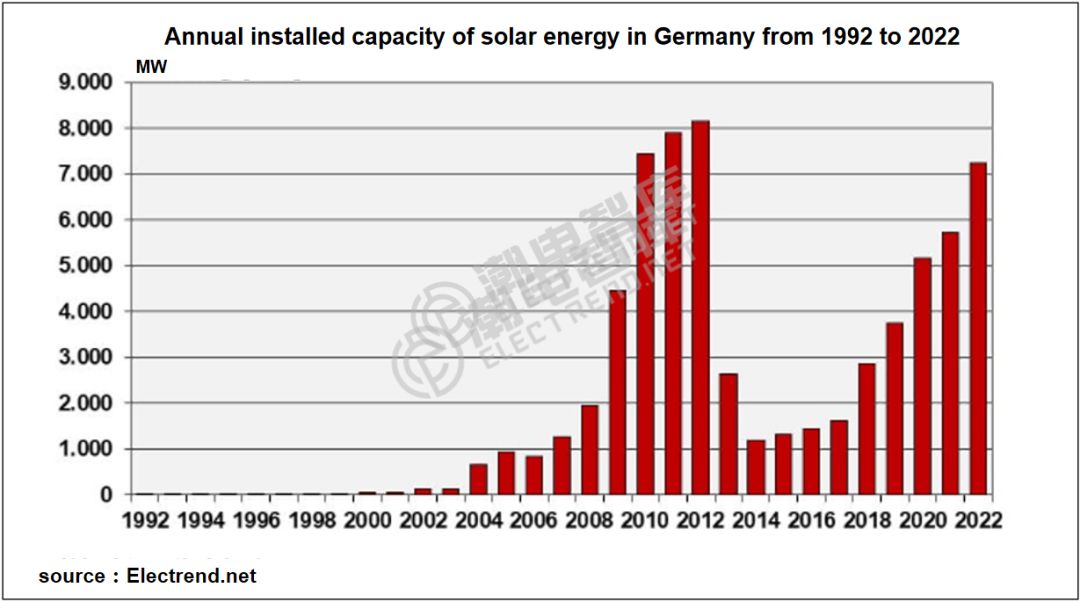

太阳能方面,由于2012年德国环境部长阿尔特迈尔的政策错误,德国太阳能产业在2012年之后一蹶不振(此前一直是世界领先),德国光伏行业破产浪潮席卷全国。

直到2022年,德国光伏市场才达到7.3GW,逐步恢复至2010-2012年的水平,但这10余年的回暖是建立在对中国的依赖下发生的。

According to Statistics by German electricity market , wind and solar energy account for more than 50% of Germany’s total electricity

Wind energy, photovoltaic and energy storage to advance side by side.

In 2022, electricity prices in Europe reached two peaks in August and December.

Between March and August 2022, electricity prices in Europe rose, reaching the first peak in August, when electricity prices in Germany more than tripled to 429 euros per 2,000 KWH. The geopolitical conflict between Russia and Ukraine has led to rising power costs, including Europe’s failure to respond to the negative effects of supply disruptions.

From September to December, electricity prices in European countries began to pay off, and electricity prices fell to the beginning of the year in October. But on September 26, the north Stream pipeline explosion once again caused electricity panic, and electricity prices rose all the way up to the second peak in December.

Since 2023, Europe’s energy transition has begun to pay results, but the EU has been divided on the development of renewable energy industry: hydrogen and wind energy have been placed at the same height as solar energy, leading to the uncoordinated development of renewable energy. The repeated rise and fall of electricity prices also reflect the conflict of energy development in Europe.

Wind and solar (photovoltaic) have become the two pillars of German power, and the proportion is increasing year by year.

Compared to 2010, German solar contribution rose from 18GW to 60.6GW, from 11% to 26%; wind contribution was 27GW to 64.5GW, from 16% to 27%. The two pillars will generate 50% more than 50% of Germany’s annual output in 2022.

In terms of wind energy, Germany’s total new installed capacity in 2022 exceeded 2.75GW for the first time since 2019, including 0.3GW offshore and 2.4GW on land.

On the solar side, the German solar industry collapsed after 2012 (previously the world leader) in 2012, and the bankruptcy of the German photovoltaic industry swept the country.

It was not until 2022 that the German photovoltaic market reached 7.3GW, gradually recovering to the level of 2010-2012, but the recovery of more than 10 years was based on the dependence on China.